Since the UAE Dirham is pegged to the US Dollar, and the Indian rupee is forecasted to marginally strengthen against the US Dollar over the coming months and gain slightly in a year as Reserve Bank of India uses its foreign exchange reserves to manage volatility and keep the currency relatively strong., the latest AED to INR forecast is pointing towards slightly lower levels in the coming months.

Unlike most emerging market currencies, the Indian rupee has showed remarkable stability against the US dollar and though against AED, thanks to the Reserve Bank of India (RBI)'s hefty foreign exchange reserves of over $619 billion, which it has used to absorb excess volatility.

While most emerging market currencies have weakened against the dollar and the dirham so far this year, the rupee has traded in a tight range of 82.64-83.45 USD and 22.53-22.76 AED and is down less than 0.5%.

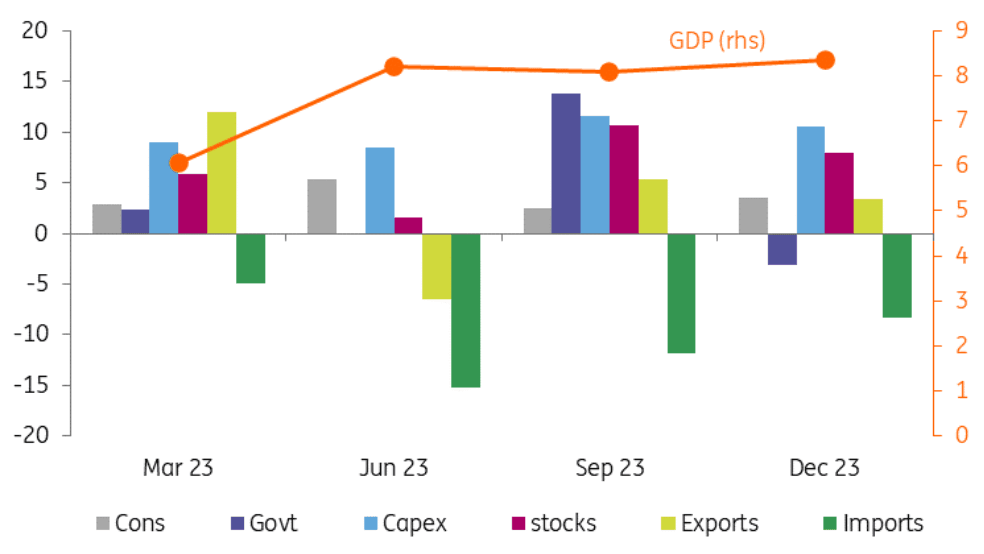

In 2023, India managed to grow 7.7%, not only beating all other major economies but exceeding the forecasting community's expectations and accelerating into the second half of the year as the rest of the world slowed.

Here we look in more detail at what has been driving the rupee price and where it may go next, including the latest AED to INR forecast for 2024, 2025, and 2030.

AED to INR Forecast – Summary

- AED to INR Forecast 2023: Although there is a good chance that India will see a similarly impressive performance this year, the latest forecasts show the Indian rupee will strengthen only marginally over the coming three months, to 22.5731 AED.

- AED to INR Forecast 2024: Growth (in the U.S.) has been holding up, which may lead the Fed to delay its rate-cut cycle, which will make the case for a stronger dollar in the near term. Still, the rupee is forecasted to gain nearly 1.1% to 22.4642 AED in six months and around 1.7% to 22.3281 AED in a year.

- AED to INR Forecast 2025-2030: While some algorithm-based currency pair forecasts AED to INR remain within a range for several years, other are pointing towards an INR strength to 21.7233 by 2025 and 19.766 by 2030.

With CAPEX.com you can trade USD/INR with tight spreads starting at 0.90 pips and 1:20 leverage.

AED to INR Forecast – Fundamental: Full Speed Ahead

India is the fastest-growing major economy in 2023. India appears to be doing well, even though others in the region appear to be having difficulties. Although the INR is one of the strongest currencies in the area, inflation is still high but is expected to decline further during the year as Indian government bonds are scheduled to be added to global indices.

Economic growth

With aggressive capital investment and infrastructure initiatives that have fostered the environment for private investment to flourish rather than discouraging it, the Union Budget of 2023 provided a firm foundation for India's robust growth in 2023.

The economy expanded by an amazing 8.4% year over year in the fourth quarter of 2023, resulting in a 7.7% annual growth rate. This exceeded even the most optimistic predictions of +7% and crushed the mainstream expectation for a downturn to 6.4%.

When analysing the factors that fuelled growth in 2023, capital investment was the most reliable source. Furthermore, this capital spending is neither especially inflationary nor likely to reverse in the next quarters if it is increasing the economy's productive capacity.

Infrastructure spending

The allocation of funds by the government to infrastructure in the Union Budget for 2023–2024 was seen as beneficial. India's growth potential is significantly increased by improved logistics and transportation, which is positively influencing private investment.

For ING analysts it looks like a good bet that this positive cycle continues in 2024–2025 because the infrastructure push was maintained in the 2024–2025 Union Budget, which was authorised in February and included a double-digit growth in government capital expenditure. Even though they have lowered their growth estimate for 2024 from 7.7% in 2023 to 6.7%, if this growth rate is realised, it will still represent a robust performance.

There is one little warning worth mentioning. In addition to the GDP report, the sectoral production measure of GDP, or more specifically, gross value added, or GVA, did demonstrate a fall in 4Q23, in keeping with the consensus estimate for GDP. Even yet, India's GVA increased at a rate of 7.2% over the course of the entire year. The stark stock-building we witnessed in the second half of the year could be the cause of the two series' discrepancy; it wouldn't be shocking to see this unwind in 2024 and bring the two series back into alignment.

Government finances

The most recent Union Budget not only supported increased capital spending but also carried on the process of reducing the fiscal imbalance. The 6.4% (%) GDP equivalent deficit target for 2023–2024 was set but given that outturns have been greater than required to meet that objective, ING's analysts think it will be surpassed, whatever the results of the final month of the fiscal year will show. Therefore, they believe that this should be doable even with an even smaller target deficit of 5.9% in 2024–2025.

If so, the debt-to-GDP ratio might continue to drop for another year. India's debt-to-GDP ratio is high—too high for an economy at this stage of development—around the mid-80% mark. Consistent increases in this percentage will free up funds for more useful uses, as debt service remains the single biggest annual expense on the budget, around equal to the whole of defence and transportation spending put together.

The existing sovereign ratings of India, which are BBB- (S&P and Fitch) and Baa3 (Moody's), all with stable outlooks, are certainly too low to discuss upgrading, but with additional improvements, this may turn into a more serious conversation.

Bond inclusion

The addition of Indian government debt to the JP Morgan Global bond index in June would be the other major development for the upcoming year.

The estimated amount of capital inflows to India that would result from this is estimated to be roughly $25 billion, and the financial account of the balance of payments may already show some indication of this.

According to ING, inflows of portfolio investment (PI) did indeed increase over the second half of 2023, as expectations of the bond inclusion grew and were then confirmed. Net portfolio investment for the full year was just under USD24bn – close to the analysts' estimations in terms of capital inflows. Net inward direct investment (DI) remained very modest.

The Indian stock market is still strong; in 2023, it increased by 18%, and is marginally higher in Q1 2024. Compared to Chinese stocks, which plummeted in 2023 but have since risen a little more recently, this performance is far stronger. The market is less hesitant to purchase Indian stocks. In comparison to the Hang Seng index, which has a PE ratio of 8.7 and a price-to-book ratio of 0.94, the Sensex index has a PE ratio of 24 and a price-to-book ratio of 3.7.

Inflation and the Reserve Bank of India

Prior to the end of the year, Indian inflation appeared to be within the RBI's target range of 2 to 6%, suggesting that policy rates may be loosened. However, unpredictable monsoons have severely impacted agriculture, driving up the cost of seasonal foods. As a result, inflation has risen above the RBI's target once more, albeit it is already starting to decline.

As the government protects people from rising energy prices, analysts expect inflation to continue declining over the second half of the year. With the release of October statistics, inflation may return to the target range as early as next month.

This will maintain real rates high and present a compelling argument for a rate cut in the first half of 2024. India's policy rate, at 6.5%, is 100 basis points lower than the US rate, supporting the INR. Compared to some of its Asian contemporaries, that spread is greater. The US economy's continued defiance of logic in failing to slow down poses the biggest risk to US rates projection and maintains the strength of the USD. Because of this, the latest AED to INR forecast is slightly bullish.

AED to INR Forecast – The Latest Calls for Central Banks

Central bank rates are reaching their peak globally, and we're already starting to see rate cuts in certain regions. Since the UAE Dirham is pegged to the US Dollar (1 AED = 0.272257 USD) like the Saudi Arabian Riyal (see also SAR to INR forecast), the FED policy expectations will highly influence the AED to INR forecast. Here's what investment banks expect from policymakers from US and India over the next few months.

Federal Reserve

The U.S. Federal Reserve is widely predicted to start reducing U.S. borrowing costs in June. But the risk the FED may not only cut rates later but also cut fewer times than currently expected is increasing. The key risk to USD to INR trajectory will be a further push back in the Fed's rate-cut cycle beyond June.

Inflation has produced several hotter-than-expected prints in 2024 in some way or another which has led the FED to dismiss any notion of imminent rate cuts. The risk in Q2 is that the hotter, seasonal factors buoying inflation, reverse. Rapidly declining inflation alongside robust jobs market significantly weakens the argument for maintaining rates at elevated levels.

In addition, the US economy is moderating – declining from annualised growth of 4.9% in Q3 to 3.2% in Q4 and on track for 2.1% in Q1 this year. Should signs of weakness appear, the Fed will be motivated to cut rates to avoid a recession.

Reserve Bank of India

The RBI is expected to cut the repo rate starting with the third quarter. The Indian rupee (INR) has been under strict control of the Reserve Bank of India (RBI) since October 2023, with the exchange rate hovering around USD/INR 83.0. Although this strategy began at a time when the US dollar was confusing expectations for some decline and instead placing pressure on developing market currencies to depreciate, the RBI has not offered any explanation for it.

In recent times, there appears to have been some asymmetric flexibility in the RBI's currency management policies. The INR has been allowed to gain very slightly when the USD has shown symptoms of weakness, and the RBI has supported the INR when the USD has rebounded and put pressure on its devaluation.

To stop the depreciation of the Indian rupee, foreign exchange reserves will need to be used as part of this currency stability. If India maintains its current level of foreign exchange reserves—currently at $642.63 —the strategy appears to be well-intentioned and even growing.

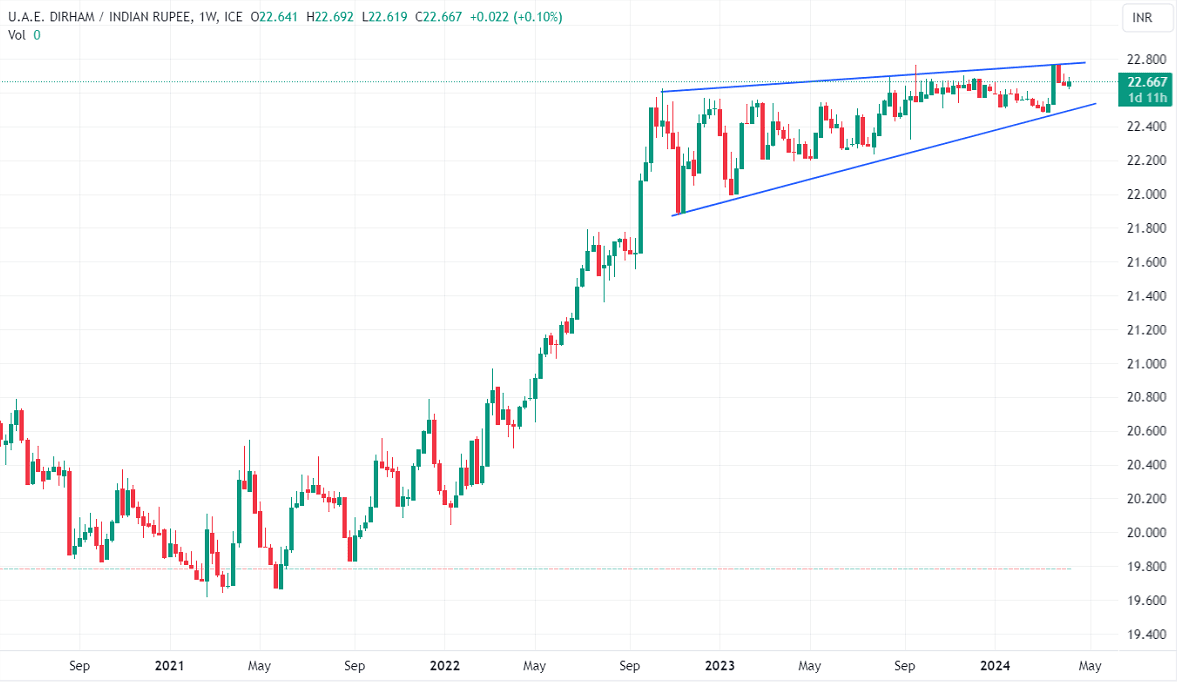

AED to INR Forecast – Technical Outlook: Rising Wedge Bearish Chart Pattern

The AED/INR upward bias remains intact as the pair holds above the key 100- and 200-day Exponential Moving Averages (EMA) on the daily chart. The immediate upside barrier to watch is seen at 22.68.

The AED to INR chart shows a rising wedge chart pattern. The rising wedge pattern typically occurs after an uptrend and signals a potential reversal in the security's price. It is a bearish chart formation commonly observed in technical analysis within the context of trading and investment. It is characterized by converging trendlines, where both the support and resistance trendlines are sloping upward, but the slope of the support line is steeper than that of the resistance line.

The rising wedge is generally considered a bearish pattern because it signals that the buying momentum is slowing down. The narrowing price range and declining volume suggest that the buyers are losing control, making it more likely for the price to break downwards.

Further north, the resistance is at 22.87, a psychological round mark at 84.00 for USD to INR pair. On the downside, a breach of the support line mark could drag the pair towards the AED to INR forecasted levels: 22.4642 AED in six months and around 22.3281 AED in a year.

In conclusion, from a technical perspective, the AED to INR forecast points toward a more likely break of the tight consolidation to trade at marginally lower levels during 2024.

AED to INR Forecast – Institutional and AI-Algorithms Price Predictions 2024, 2025, 2030

Below is the updated data of the AED to INR forecasts as of April 2024. It either can be altered or can be proved to be wrong as it is based on essential factors like interest rates and central bank policy, in line with market assumptions. It is important to research and analyse keeping in mind that past displays do not assure future outcomes.

AED to INR Forecast by Reuters Poll – Indian Rupee to rise marginally

The rupee was expected to gain slightly to 83.11/$ in a month and 82.90/$ in three months, Reuters poll of 46 foreign exchange analysts showed. That outlook has remained unchanged for several months and has been unaffected by the greenback's relative strength so far this year.

Growth (in the U.S.) has been holding up, which may lead the Fed to delay its rate-cut cycle, which will make the case for a stronger dollar in the near term. Still, the rupee is forecasted to gain slightly to 22.5731 AED in three months, nearly 1.1% to 22.4642 AED in six months and around 1.7% to 22.3281 AED in a year.

AED to INR Forecast by CareEdge Ratings: RBI to Keep Rupee Range Bound against the Dollar

As crude oil prices are expected to stay elevated in the near term, CareEdge revised their projections for India’s current account deficit (CAD) by 20bps to 1.8% of GDP in FY24 from 1.6% projected earlier. This is still lower than CAD of 2% in FY23.

Their projection assumes the Indian crude oil basket would average USD 87 per barrel in FY24 versus USD 85 per barrel assumed earlier. India’s net foreign direct investment (FDI) inflows have fallen to ~USD 5 billion in Q1FY24 from ~USD 13.4 billion in Q1FY23.

They expect FDI flows to moderate in FY24, as businesses delay investments amidst a global slowdown. Elevated UST yields and strong Dollar Index are weighing on foreign portfolio investments (FPI). India’s net FPI inflows fell to USD 2.2 billion in August from USD 5.8 billion in July and a peak of USD 6.9 billion in June.

September has seen net FPI outflows of USD 0.5 billion so far. We expect FPI flows to gain momentum once the Fed signals that interest rates have peaked. They maintain the initial view that India will witness net FPI inflows in FY24 as UST yields moderate eventually and as India benefits from favourable growth differentials arising from being the fastest-growing major economy.

In the last two MPC meetings, RBI has emphasized its commitment to bring inflation to its 4% target. Hence, we expect RBI to intervene to contain rupee volatility and imported inflation. India has adequate forex reserves, equivalent to an import cover of ~11 months, to support RBI intervention. Further, RBI’s forward book position looks comfortable at net purchases of USD 19.5 billion as of July 2023.

Elevated UST yields, weak yuan and crude oil prices are expected to weigh on rupee in the near term. Thereafter, some moderation in UST yields and crude oil prices should offer support.

In the coming second half of the fiscal year 2023-24, they forecast USD to INR exchange rate to fluctuate within the range of 82 to 84, gradually gravitating toward the lower boundary of this range. This projection marks a shift from their previous forecast of 81 to 83.

Though, the agency forecast AED to INR to trade within the 22.325-22.87 range within the next 6 month.

AED to INR Forecast by ING

Analysts forecast USD to INR has some downside potential (INR appreciation) when the USD finally does turn weaker is more limited than some other currencies, as the currency is currently only supported in a narrow range and has not seen the same level of depreciation as other regional currencies.

As a results, the ING's AED to INR forecast for the beginning of 2024 is 22.46. The AED to INR forecast for the next 12 month is 22.052.

AED to INR Forecast by Trading Economics

Trading Economics forecast AED to INR to be priced at 22.7890 by the end of Q2 2024 and at 23.0636 in one year, according to its global macro models projections and analysts' expectations.

AED to INR Forecast by Wallet Investor

Wallet Investor forecast AED to INR to close 2023 at 22.727 and expects a Dirham appreciation during the next year.

The 2024 AED to INR price prediction towards a all-time high of 24.038, and a closing rate of 23.81. The 2025 AED to INR forecast is showing a potential maximum rate of 25.125 and a closing rate of 25.00. The AED to INR forecast for the next 5 years is bullish, with the AI algorithm predicting a new all-time high of 28.98.

AED to INR Forecast 2025 by AI Pickup

The Artificial Intelligence (AI) Pickup algorithm supports the statement that the strength of the prevailing trend and the live inflationary climate will continue to weaken the rupee in a long-term forecast until 2027. The AI algorithms AED to INR forecast 2025 points towards an advance up to 24.28.

Summary of AED to INR Forecast

- The Indian Rupee has recently breached the 83-level against the US Dollar and 22.297 against the AED, but its decline has been curtailed by interventions by the Reserve Bank of India (RBI) across various markets, including the spot, Non-Deliverable Forward (NDF), and futures markets.

- In the coming second half of the fiscal year 2023-24, most institutions and AI-algorithms forecast the USD to INR exchange rate to fluctuate within the range of 82 to 84, gradually gravitating toward the lower boundary of this range. Though, AED to INR forecast is a trading range within the 22.325-22.87 levels.

Sources:

- https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx

- https://static.pib.gov.in/WriteReadData/specificdocs/documents/2024/feb/doc202421304601.pdf

- https://www2.deloitte.com/us/en/insights/economy/asia-pacific/india-economic-outlook.html

- https://www.goldmansachs.com/intelligence/pages/gs-research/india-2024-outlook-port-of-calm-in-a-higher-for-longer-world/report.pdf

- https://www.morganstanley.com/im/publication/insights/articles/article_theindiaopportunity_ltr.pdf